- Standard processors prohibit vape and tobacco sales in their terms of service even if you’re compliant

- High-risk merchant accounts are the only reliable path to stable, long-term card processing

- Chargebacks, regulatory scrutiny, and age-verification requirements are the three core reasons banks flag vape businesses

- Approval is possible – typically within 3-5 business days with the right specialized processor

- Post-approval shutdowns are a real and common threat if your processor doesn’t truly understand the industry

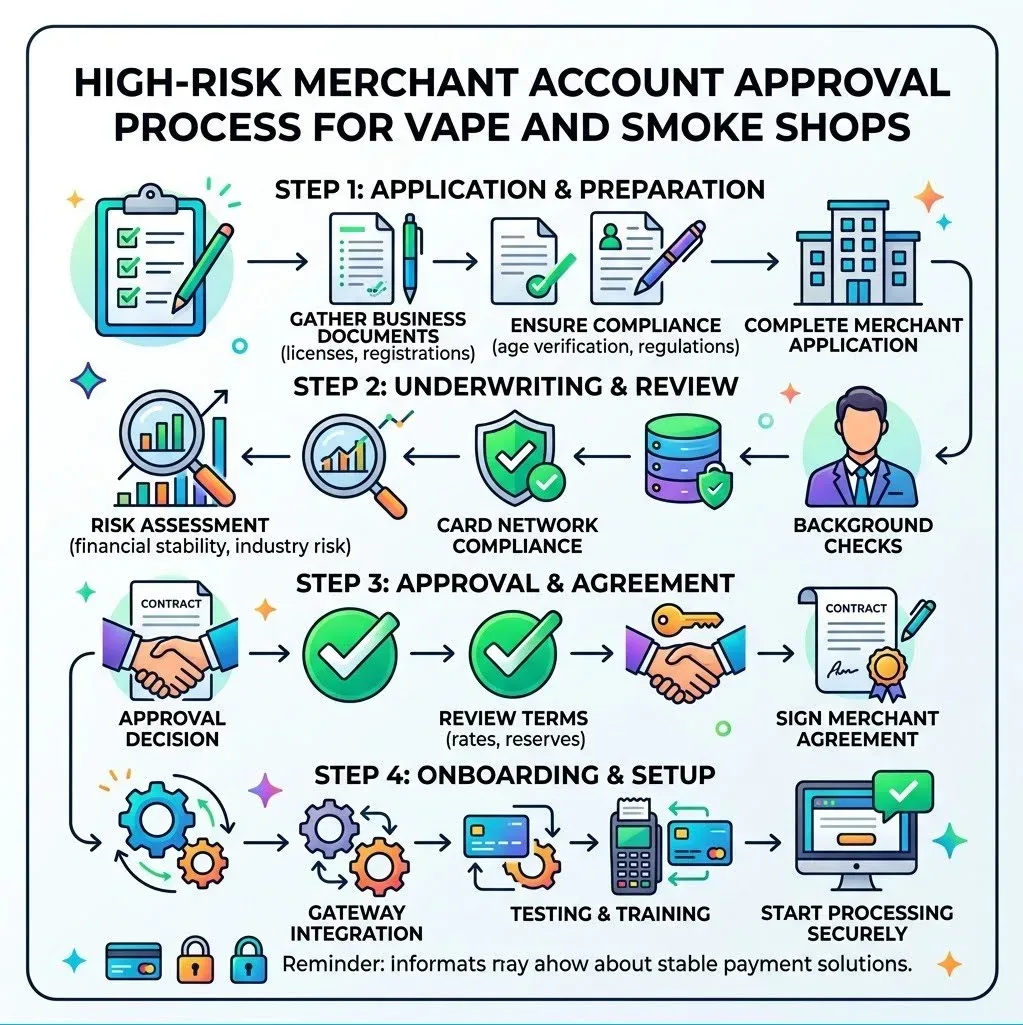

Step-by-step process for getting approved for smoke shop payment processing

Why Smoke Shops (Including Vape) are Classified as High-Risk

When we talk to shop owners in Boston and across the country, the first question is always: “Why me?” You’re running a clean shop, paying your taxes, and following the rules. Yet, the banking world treats you like a “vice” industry. The classification of high risk vape shop payments stems from three main pillars: regulatory volatility, reputational risk, and financial liability.Regulatory Uncertainty and the FDA

The vaping industry exists in a state of constant flux. Between the FDA’s Premarket Tobacco Product Application (PMTA) process and evolving state-level flavor bans, banks are terrified of “future sanctions.” They worry that a sudden federal ruling could overnight make your inventory illegal, leading to a massive wave of chargebacks or business failures. This is why specialized High Risk Regulated processing is non-negotiable.The PACT Act and Shipping Restrictions

If you sell online, the Pact Act changed everything. It imposed strict requirements on how tobacco and vape products are shipped, taxed, and age-verified. Mainstream processors don’t want the headache of auditing whether you are collecting the correct excise taxes for a customer in another state.High Chargeback Ratios

Vape shops often see higher-than-average dispute rates. This can be due to “friendly fraud” (customers claiming they didn’t receive a package), underage buyers using a parent’s card, or simply a lack of billing clarity. In the first half of 2025 alone, credit card fraud cases in the US hit over 323,000 – a 51% increase from the previous year. For a bank, a chargeback ratio above 1% is a “red alert” that can lead to immediate account termination.

Tablet-based POS systems support flexible smoke shop payment processing

- Age-Gated Products: Anything requiring ID verification is automatically flagged

- Health Claims: Any perceived association with health risks makes banks nervous

- Online Sales Scrutiny: Card-not-present transactions are inherently riskier

- Industry Stigma: Some banks simply refuse to support Tobacco Payment Processing due to internal “reputational risk” policies

Navigating High-Risk Smoke Shop Payments and Compliance

In 2026, compliance isn’t just about following the law; it’s about protecting your ability to take money. If your payment gateway isn’t synced with your compliance tools, you are one audit away from a shutdown.The PMTA and Your Merchant Account

The FDA’s PMTA process requires detailed product submissions, including ingredients and scientific evidence of health impacts. While you might think this is just a manufacturing issue, processors look for PMTA compliance during underwriting. If you are selling products that haven’t cleared these hurdles, your Vape Ecigarette Payment Processing account could be at risk.Age Verification and ID Scanning

For in-store sales, simple visual ID checks are no longer enough for high-risk processors. We recommend integrated ID scanning that logs the verification. For online sales, AI-powered age verification (which matches ID uploads to face scans) is becoming the industry standard. This doesn’t just keep you legal; it provides a “paper trail” to fight chargebacks from parents claiming their child made an unauthorized purchase.Understanding MCC 7120 and ENDS

Merchant Category Codes (MCC) are how banks identify your business. Vape products often fall under Electronic Nicotine Delivery Systems (ENDS). Using the wrong code (like “General Retail”) might get you lower rates initially, but it is considered “merchant identity suicide.” When the bank finds out, they won’t just close your account; they’ll blacklist you.PCI DSS and Tokenization

Security is paramount. Every smoke shop must be PCI DSS compliant. We utilize tokenization, which replaces sensitive card data with a unique “token.” This means if your system is ever breached, the hackers get useless strings of code, not your customers’ credit card numbers.Mitigating Chargebacks in High-Risk Smoke Shop Payments

A single bad month of disputes can kill your business. For high-risk merchants, a chargeback ratio exceeding 1% is the “danger zone.” Here is how we help our partners stay below that threshold.Clear Billing Descriptors

The number one cause of “friendly fraud” is a customer not recognizing the charge on their statement. If your shop is “Cloud Nine Vapes” but your billing descriptor says “CNV Holdings LLC,” the customer will dispute it. Ensure your descriptor matches your storefront name exactly.Robust Refund Policies

Make it easier for a customer to get a refund from you than to call their bank. A clear, prominent refund policy reduces the incentive for a customer to initiate a chargeback.Fraud Detection and 3D Secure

Implement tools like 3D Secure, which adds an extra layer of verification for online transactions. Combined with Address Verification Service (AVS) and Card Verification Value (CVV) checks, these tools stop most fraudulent attempts before they happen.Proactive Dispute Representment

When a chargeback does happen, you need to fight it. Having a specialized processor means having access to experts who know how to present evidence like delivery confirmation and signed age verification to win back your funds.Future Trends in High-Risk Smoke Shop Payments

The landscape of high risk vape shop payments is shifting toward automation and transparency. By 2037, the global market is projected to be worth over a trillion dollars, and the technology is evolving to match that scale.- AI Verification: We are seeing AI that can predict fraudulent transactions based on buying patterns before the “Buy” button is even clicked

- Blockchain Authenticity: Blockchain is being used to track the supply chain of e-liquids. Customers can scan a QR code to verify the product’s authenticity, and that same blockchain record can be used to verify the transaction to the bank

- Smart Contracts: In the future, funds might be held in smart contracts that only release to the merchant once age verification and delivery are cryptographically confirmed, virtually eliminating “item not received” disputes

Essential Features of a Specialized Smoke Shop Merchant Account

Don’t be fooled by “instant approval” promises. In the high-risk world, if the underwriting isn’t rigorous at the start, the shutdown will be rigorous at the end.Upfront Underwriting

A legitimate Smoke Shop Credit Card Processing provider will ask for a lot of paperwork: bank statements, ID, business licenses, and processing history. This is a good thing. It means they are actually “underwriting” your business so they can defend it to the bank later.Rolling Reserves

Many high-risk accounts require a “rolling reserve” — a small percentage of your daily sales held for a set period (usually 6–12 months) to cover potential chargebacks. While it affects cash flow, it provides a safety net that keeps the bank comfortable with your business.Settlement Speeds and Fast Funding

In a high-volume retail environment, you can’t wait 10 days for your money. We prioritize fast funding, often providing next-day deposits for qualified merchants. This stability allows you to restock inventory and grow without cash flow bottlenecks.Transparent Rates

Mainstream processors often hide fees in “tiered” pricing. For Smoke Shop Credit Card Processing, you want interchange-plus pricing. This is the most transparent model, showing you exactly what the card networks charge and what the processor is taking.

Reliable card terminals are essential for smoke shop payment processing

Integrating POS Systems and Alternative Payment Methods

Your Point of Sale (POS) system is the heart of your operation. It’s not just for ringing up sales; it’s for managing the unique risks of the smoke shop industry.| Feature | Online Sales Risk | In-Store Sales Risk |

|---|---|---|

| Age Verification | High (Requires AI/ID Upload) | Low (Physical ID Check) |

| Fraud Risk | High (Stolen Cards/Botting) | Low (Card Present/EMV) |

| Chargeback Rate | Typically Higher | Typically Lower |

| Compliance | PACT Act / Shipping Laws | Local Zoning / FDA |

Cloud Inventory and IoT

Modern Smoke Shop Payment Processing integrates with cloud-based inventory. Some shops are even using IoT “smart shelves” that alert you when stock is low, ensuring you never miss a sale on a high-margin item.Smoking Accessories and Hardware

If you sell high-end glass or expensive mods, your Smoking Accessories Payment Processing needs to handle high-ticket transactions. A $500 sale is flagged differently than a $20 juice sale. Your merchant account must be configured to handle these “velocity spikes” without freezing your funds.Alternative Payments

- Mobile Wallets: Apple Pay and Google Pay are essential for speed and security

- Cryptocurrency: For some online vape shops, crypto offers a way to bypass traditional banking hurdles entirely, though it requires its own compliance framework

Avoiding Post-Approval Shutdowns and Frozen Funds

The “Mainstream Processor Horror Story” is common: You get approved in five minutes, process $20,000 in sales, and then receive an email saying your account is closed and your funds are held for 180 days.Why Shutdowns Happen

Most mainstream processors use “automated” underwriting. They don’t actually look at your business until you hit a certain volume or get your first chargeback. When a human finally looks and sees “Vape Shop,” they pull the plug.Disruption Prevention

To ensure account longevity, you must be transparent. If you’re planning a massive “Buy One Get One” promotion that will triple your volume, tell your processor. If you’re adding Tobacco Credit Card Processing or Processing Payments For Tobacco Pouches to your product line, update your account.The MATCH List

The worst-case scenario is being placed on the MATCH list (Member Alert to Control High-risk). This is a “blacklist” shared by banks. If you are on this list, getting a merchant account anywhere becomes nearly impossible for five years. Working with a specialized high-risk provider is the best way to stay off this list.Frequently Asked Questions about Smoke Shop Payments

Why is specialized high-risk payment processing essential for smoke and vape shops?

Standard processors explicitly forbid vape sales in their fine print. Using them is like building a house on sand; eventually, the tide comes in, and they will shut you down, often holding your funds for months. A specialized account is underwritten specifically for your industry’s risks.What is the impact of the PMTA on my merchant account stability?

Processors and banks monitor FDA enforcement. If you are selling “unauthorized” products that the FDA has issued Warning Letters for, a bank may view your business as a legal liability and terminate your processing to avoid “aiding and abetting” illegal sales.How long does it take to get approved for a high-risk account in 2026?

While “low-risk” accounts are instant, a solid high-risk account usually takes 3 to 5 business days. This time is spent by human underwriters verifying your business license, your age verification steps, and your financial stability to ensure that once you are approved, you stay approved.Conclusion

At Vector Payments, we don’t believe that “high-risk” should mean “high-stress.” We understand the US smoke shop market and the national vape landscape better than anyone. We’ve built our reputation on providing a stable, long-term business partnership rather than just a transaction. We offer the best of both worlds: the robust security and compliance of a high-risk specialist, with the transparent, low-risk pricing and 7-day support you’d expect from a premium fintech partner. Stop worrying about when the “shutdown email” is coming. Focus on growing your shop, and let us handle the infrastructure to simplify the payments experience!Ready to Secure Your Smoke Shop Payment Processing?

Stop worrying about when the “shutdown email” is coming. Focus on growing your shop, and let us handle the infrastructure to simplify the payments experience.

Secure Your Stable Smoke Shop Payment Processing