- You’re classified as high-risk: Banks and card networks apply stricter scrutiny to smoke shops from day one

- Friendly fraud is rampant: Customers dispute legitimate purchases, especially on higher-ticket items like glassware and vaporizers

- Age-restricted products create confusion: Shipping restrictions and compliance gaps lead to more disputes

- Generic processors aren’t built for you: They panic at small dispute spikes and often don’t fight chargebacks on your behalf

- Your chargeback ratio target is under 1%: Calculated as total disputes ÷ total transactions (e.g., 10 disputes on 800 transactions = 1.25%, which puts your account at risk)

- The fastest wins: clear billing descriptors, a visible refund policy, AVS/CVV fraud checks, and a specialized high-risk processor that actually submits dispute evidence

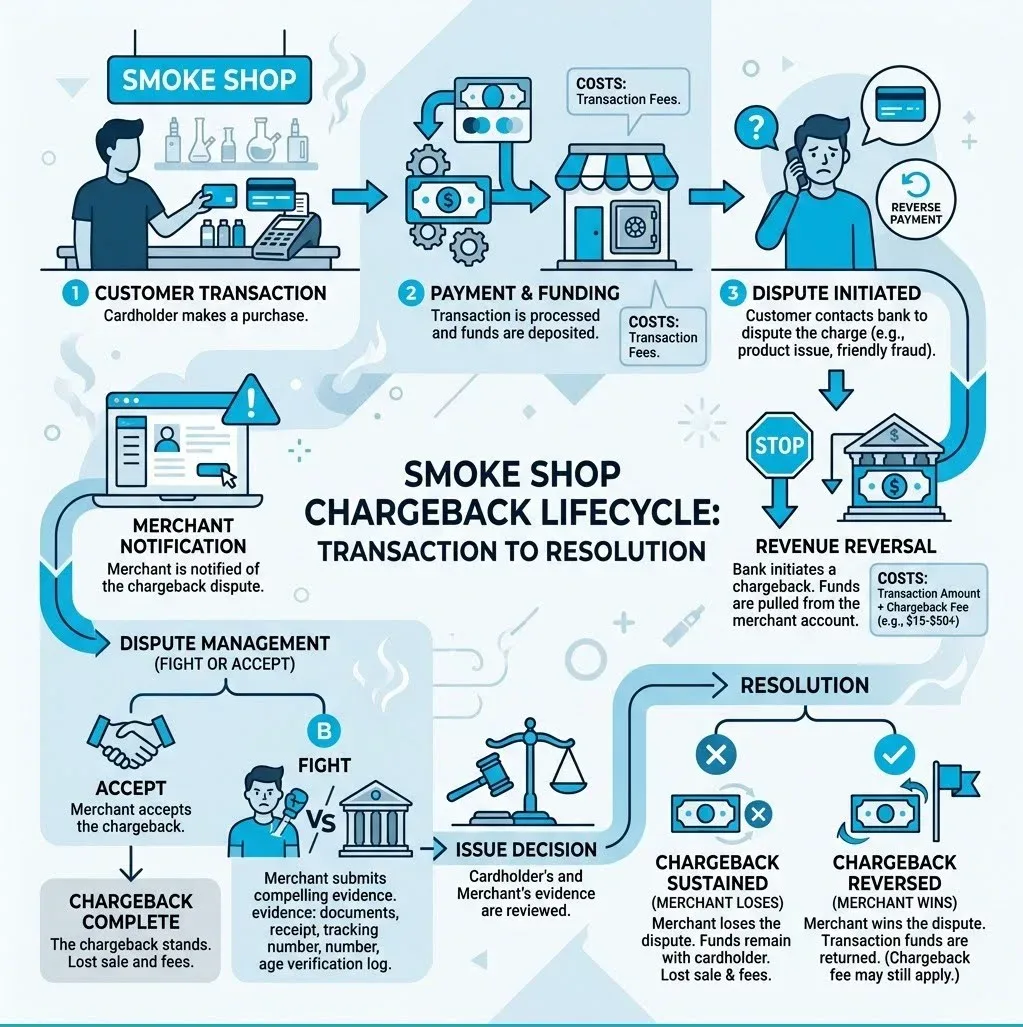

Understanding the full chargeback lifecycle is key to reducing disputes in smoke shops

Calculating Your Ratio: Why Smoke Shop Chargebacks are High Targets for Banks

Banks don’t look at the dollar amount of your chargebacks as much as they look at your “chargeback ratio.” This is the primary metric used to determine if your business is “too risky” to keep around. To calculate your ratio, take the number of chargebacks in a given month and divide it by the total number of transactions processed in that same month. For example, if you have 10 disputes and you processed 800 transactions, your ratio is 1.25%. While 1.25% might sound small, in high-risk processing, it is a flashing red light. Most processors want to see you well under 1%, especially with the recent VAMP changes occurring. If you cross that line, you aren’t just paying fees; you are risking a total freeze of your funds. Understanding this math is the first step in chargeback prevention, allowing you to spot trends before the bank does.Managing the Operational Costs When Smoke Shop Chargebacks are High

The damage of a chargeback goes far beyond the lost sale. When a dispute is filed, you are hit with a non-refundable chargeback fee, typically ranging from $20 to $100 per incident. Think about the math: If you sell a $50 vaporizer and the customer files a chargeback, you lose:- The $50 retail price of the item

- The wholesale cost of the inventory (which you can’t get back)

- The original shipping costs

- A $50 chargeback fee from your processor

Secure and approved payment processing for smoke shop transactions

Essential Fraud Prevention Tools for High-Risk Smoke Shops

To protect your revenue, you need more than just a standard credit card reader. You need a defensive perimeter built on modern security protocols. For online sales, this means utilizing Address Verification Service (AVS) and Card Verification Value (CVV) checks. These tools ensure that the person making the purchase actually possesses the card and knows the billing address associated with it. In-store, the stakes are just as high. We’ve seen cases where even employees are involved in fraudulent transactions, highlighting the need for robust internal controls and secure smoke shop credit card processing.The Role of Age Verification in Fraud Mitigation

Age verification is the backbone of compliance for any smoke or vape shop. In 2026, relying on a simple “Are you 21?” pop-up is no longer sufficient. Modern vape and e-cigarette payment processing requires integrated ID software that verifies a customer’s identity against public records or government-issued IDs in real-time. This doesn’t just keep you on the right side of the PACT Act and FDA regulations; it also acts as a powerful deterrent against fraud. Most “friendly fraudsters” or teenagers using a parent’s card will abandon a cart the moment they are asked to upload a photo of their ID. By implementing strict age verification, you filter out high-risk transactions before they ever reach your merchant account.Implementing EMV and PIN Technology

If you are still swiping cards or entering numbers manually for in-store purchases, you are essentially inviting chargebacks. Since the EMV liability shift, merchants who do not use chip readers are held 100% responsible for any fraudulent “card-present” transactions. By using specialized smoking accessories payment processing hardware that supports EMV and PIN entry, you shift that liability back to the card-issuing bank. If a customer chips their card and enters a PIN, it becomes almost impossible for them to later claim the transaction was “unauthorized.”Operational Strategies to Mitigate Friendly Fraud

“Friendly fraud” is when a legitimate customer makes a purchase but later disputes it with their bank. Sometimes they do this maliciously to get free products, but often it happens because they don’t recognize the charge on their statement or they are unhappy with the product and find a chargeback easier than a return. Proper tobacco payment processing involves setting up operational barriers that make it harder for customers to “accidentally” file a dispute.Optimizing Billing Descriptors to Prevent Confusion

One of the most common reasons smoke shop chargebacks high rates exist is a cryptic billing descriptor. If your shop is named “The Cloud Palace” but your bank statement shows up as “CP Holdings LLC,” your customer might see that charge three weeks later and have no idea what it is. Their first instinct? Call the bank and report fraud. You must ensure your billing descriptor is clear and recognizable. It should ideally include your store name and a phone number. For businesses using nicotine merchant services, a descriptor like “CLOUD-PALACE-SMOKE-800-555-0199” is far more effective at stopping “I don’t recognize this” disputes than a generic corporate name.Establishing Clear Purchase and Refund Policies

Ambiguity is the enemy of the merchant. If your refund policy is buried in fine print or isn’t posted at the register, a customer who receives a faulty coil might jump straight to a chargeback because they don’t think you’ll help them. Whether you are processing payments for tobacco pouches or high-end glass, your policies should be:- Prominent: Posted at the POS and on every page of your website

- Explicit: “All glass sales are final” or “Returns accepted within 14 days with original packaging”

- Documented: Include your refund policy on every digital and physical receipt

Building a Chargeback Evidence Kit to Protect Your Revenue

When a chargeback does happen, the burden of proof is on you. You are essentially “guilty until proven innocent” in the eyes of the card networks. To win, you need to provide a compelling “evidence kit” that proves the transaction was legitimate and that you followed all protocols. Keeping organized records of your chargeback time limits is vital to ensuring you respond before the window closes.Essential Documentation for Dispute Resolution

To fight a chargeback effectively, you should be able to produce the following for every high-value transaction:- Signed Receipts: For in-store purchases, a physical or digital signature is gold

- Tracking Numbers: Proof that the item was delivered to the address provided

- Adult Signatures: For shipped tobacco or vape products, a “signature required” delivery is the strongest evidence of receipt

- Customer Communication: Emails or chat logs showing the customer was satisfied or asked questions about the product

Winning Disputes with Specialized Processor Support

Generic, low-risk processors often provide zero help when it comes to disputes. They might send you an automated email, but they won’t help you build a case. A specialized high-risk provider offers chargeback protection solutions that include:- Dispute Alerts: Notifying you before a dispute becomes a formal chargeback so you can issue a refund and avoid the fee

- Underwriting Alignment: Ensuring your business is coded correctly so the bank expects the occasional dispute

- Automated Evidence Submission: Helping you compile the right data to win your case

The 30-60-90 Day Action Plan for Reducing Chargebacks

Reducing your chargeback rate isn’t an overnight fix; it’s a process of hardening your business against risk. If you’ve found your smoke shop chargebacks high lately, follow this phased approach to stabilize your smoke shop credit card processing.Days 1-30: Policy Stabilization and Staff Training

The first month is about closing the obvious loopholes.- Update Signage: Place your refund and return policy clearly at the checkout counter

- Staff Training: Teach your team how to handle “unhappy” customers. Give them a script that encourages a store credit or a refund over a bank dispute

- ID Verification: Ensure every single employee knows how to use your ID verification tools without exception. This is the core of smoke shop payment processing safety

Days 31-90: Technical Optimization and Processor Evaluation

Once the “human” element is handled, move on to the technical side.- Audit Descriptors: Check your bank statements to ensure your store name and phone number appear exactly as they should

- Tighten AVS/CVV Rules: In your online gateway, set your fraud filters to “Strict.” It’s better to lose a single suspicious sale than to deal with a $100 chargeback fee later

- Evaluate Your Processor: If your current processor is still charging you high fees and offering no support during disputes, it’s time to move to a high-risk specialist who understands the tobacco and vape industry

Frequently Asked Questions about Smoke Shop Chargebacks

What is the ideal chargeback ratio for a smoke shop?

While low-risk businesses can sometimes hover around 1%, a smoke shop should aim for well under 1%. Ideally, you want to stay at 0.5% or lower. If you hit 1%, most high-risk processors will put you on a “probationary” status. If you stay there, they will likely terminate your account.How do specialized smoke shop processors differ from generic ones?

Generic, low-risk processors often have “no-tobacco” clauses in their terms of service. They might let you process for a few months, but once they audit your account or see a few chargebacks, they will shut you down and freeze your funds for 180 days. Specialized processors like Vector Payments understand the industry, offer higher dispute thresholds, and provide 7-day support to help you manage risks.Can I get my merchant account back after a shutdown?

Reinstating an account with a processor that has already terminated you is very rare. Usually, the best course of action is “reboarding” with a new sponsor bank that is specifically chosen for your product mix (CBD, Kratom, Vape, etc.). Transparency is key here. Never try to hide your product list from a new processor.Ready to Protect Your Smoke Shop From Chargebacks?

Stop letting friendly fraud and rising dispute ratios put your merchant account at risk. Partner with a processor that actually fights chargebacks on your behalf.

Secure Your Smoke Shop Payment Processing